Monday, July 7, 2014

Saturday, May 3, 2014

Real Estate: We are NOT the Only Ones Saying You Should Buy

We have never hid our belief in homeownership. That does not mean we think EVERYONE should run out and buy a house. However, if a person or family is ready, willingand able to purchase a home, we believe that owning is much better than renting. And we believe that now is a great time to buy.

We have never hid our belief in homeownership. That does not mean we think EVERYONE should run out and buy a house. However, if a person or family is ready, willingand able to purchase a home, we believe that owning is much better than renting. And we believe that now is a great time to buy.

We are not the only ones that thinkowning has massive benefits or that now is a sensational time to plunge into owning your own home. Here are a few others:

Benefits of Owning

“Homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord…Having to make a housing payment one way or the other, owning a home can overcome people’s tendency to defer savings.”

“Renters have much lower median and mean net worth than homeowners in any survey year.”

Benefits of Buying Now

“Buying costs less than renting in all 100 large U.S. metros… Now, at a 30-year fixed rate of 4.5%, buying is 38% cheaper than renting nationally.”

"One thing seems certain: we are not likely to see average 30-year fixed mortgage rates return to the historic lows experienced in 2012…Yes, rates are higher than they were a year ago – and certainly higher than two years ago. But if you look at the averages over the last four decades, today's rates remain historically low."

Friday, May 2, 2014

14302 ASTRODOME DR #74, SILVER SPRING, MD 20906

14302 ASTRODOME DR #74, SILVER SPRING, MD 20906

|

Overview Maps Photos Features Description Video Market Report Neighborhood Market Stats |

|

|

Sirous M Jafari

Real Pros (301) 881-2000 sirous@realprosdc.com http://www.realestatefreesearch.com/ Listed by: Real Pros |

Nearby properties for sale |

Sunday, April 13, 2014

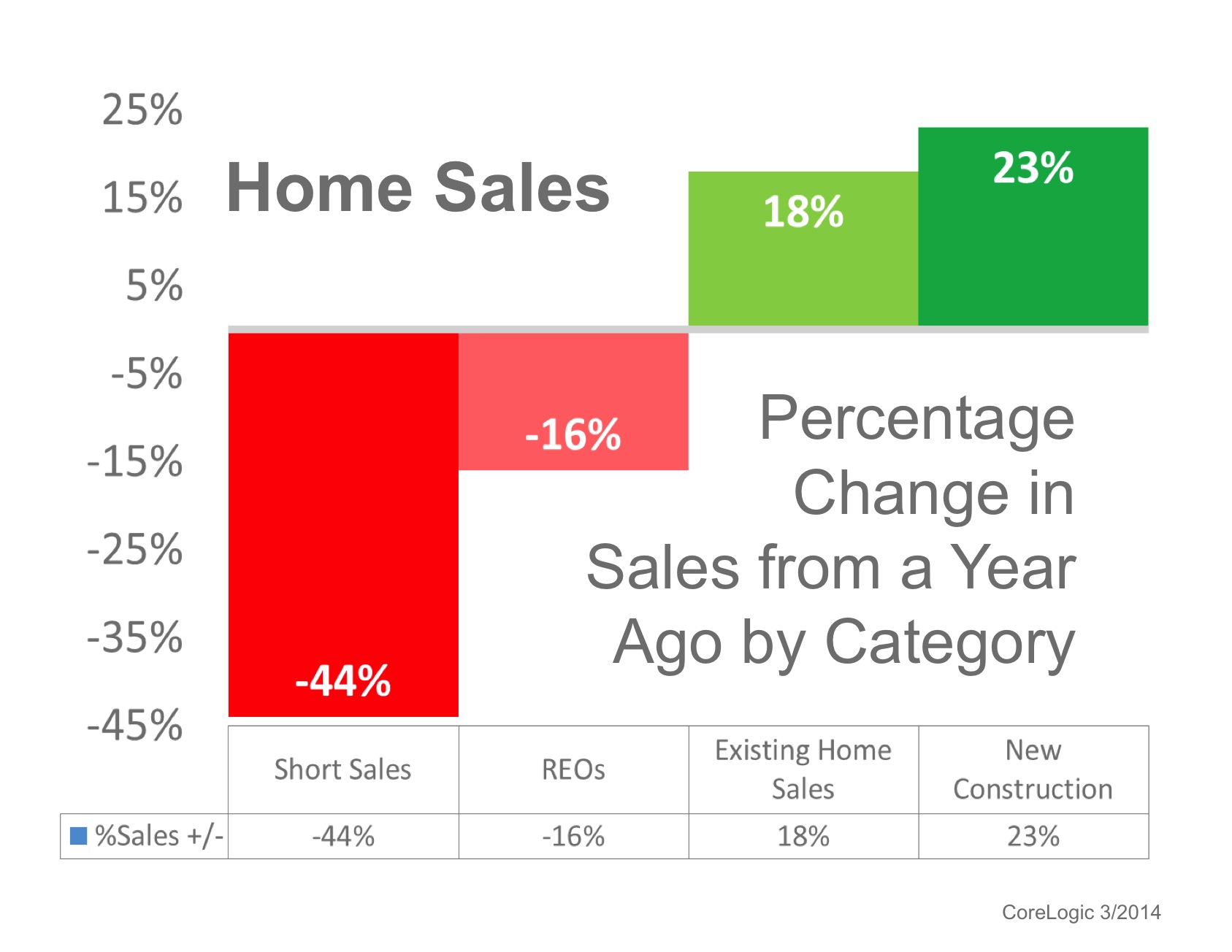

Speak Intelligently about the Home Sales Numbers

It is crucially important that, as experts in the real estate field, we can articulate what is actually taking place in the housing market…especially when news headlines are causing confusion. That is definitely the case right now when it comes to existing home sales numbers.

Overall, sales volumes are down. We realize that. However, a closer look at the numbers show that certain categories and price ranges are down while others are up.

Below is CoreLogic’s breakdown of recent sales compared to last year by category. As we can see, distressed property sales are down while non-distressed property sales are up.

Sunday, February 2, 2014

Predictions for 2014: Sales Will Surge

Many housing pundits are calling for home sales to do slightly better in 2014 than they did in 2013. To the contrary, we strongly believe that home sales will skyrocket with increases of 10-15% in 2014. Here are the three categories of buyers we believe will create this strong demand.

Many housing pundits are calling for home sales to do slightly better in 2014 than they did in 2013. To the contrary, we strongly believe that home sales will skyrocket with increases of 10-15% in 2014. Here are the three categories of buyers we believe will create this strong demand.The First Time Buyer

The Urban Land Institute recently released a report, Emerging Trends in Real Estate 2014, projecting that 4.48 million new households will be formed over the next three years. Millennials will make up a large portion of these new households. With the economy improving, we believe they will finally be moving out of their parents’ homes and, when they compare renting versus buying, many will choose homeownership.

The Move-Up Buyer

Over the last several years many homeowners were trapped in their home by negative equity. This prevented them from moving up to the home of their dreams. Zillow has justrevealed that home equity increased by $1.9 trillion dollars in 2013 an increase of 7.9% in the last twelve months. With home values rising, this pent-up demand will finally be released and move-up properties will be in high demand.

The Immigrant Buyer

No one knows what will happen with immigration reform. However, we do know what such reform would have on housing demand. A recent study released by the Immigration Task Force of the Bipartisan Policy Center (BPC) found that immigration reform, if passed, would dramatically increase demand for housing units; increasing residential construction spending by an average of $68 billion per year over the next 20 years.

We realize that our projections are based on three situations that are still uncertain. However, we believe that these issues will come to fruition and thereby dramatically increase demand for homeownership.

Friday, January 31, 2014

Read the Fine Print in Your Retirement Plan

|

||||||||||

|

|

|||||||||||||||||||||||

|

|||||||||||||||||||||||

|

|||||||||||||||||||||||

| |||||||||||||||||||||||

Wednesday, January 29, 2014

Predictions for 2014: Interest Rates Will Increase Significantly

Most experts are calling for an increase in mortgage interest rates in 2014. However, we believe the increase will be more dramatic than is being projected. We believe rates will be closer to 6% than 5% by year’s end.

The Fed announced last month that they would be pulling back some of their stimulus package which has helped the housing market by keeping long term mortgage rates at historic lows for the last few years. This should come as no surprise as the KCM Blog has been warning of this likelihood over the last several months.

Above are the most recent projections of where rates will be at the end of 2014 by the four major agencies. However, we believe that the government is not afraid to shoot right past these levels.

Doug Duncan, chief economist for Fannie Mae, this past summer announced:

“I don’t think the Fed ultimately would be troubled with a 6.5% mortgage rate.”

And Frank Nothaft, Freddie Mac VP and chief economist, at virtually the same timeexplained:

"As the economy continues to improve, we expect to see continued upward movement in long-term interest rates… At today’s house prices and income levels, mortgage rates would have to be nearly 7 percent before the U.S. median priced home would be unaffordable to a family making the median income in most parts of the country.”

Only time will tell. However, we feel that rates will be in the 5.75-6% range by year’s end.

Subscribe to:

Posts (Atom)